Your Business Is Profitable. So Why Aren’t You Building Wealth?

The gap between a thriving P&L and a growing net worth isn’t an accident, it’s a structural problem most entrepreneurs never fix.

You cleared $400,000 last year. Maybe $800,000. The business is real, the revenue is growing, and the clients are paying. And yet, when you sit down and look at your actual financial picture, your investments, your net worth outside the business, your retirement accounts, the number staring back at you is embarrassing.

This isn’t a cash flow problem. It’s a design problem.

Most profitable businesses are built to generate income, not to build wealth. Those are two different machines. Income flows through your life. Wealth compounds outside it. And if you’ve never deliberately built the second machine, you’re running on a treadmill, fast, sweating, going nowhere.

Here’s what’s actually happening, and how to fix it.

Most entrepreneurs overpay taxes not because they earn too much, but because they plan too late.

The Premium Newsletter delivers one actionable tax strategy every week: entity structures, retirement account moves, and deductions most CPAs don’t mention until it’s too late to use them. No fluff, no generic advice, just strategies you can bring to your accountant on Monday.

One implemented strategy will likely pay for the subscription many times over.

The tax bill is eating your compounding window

When you take money out of your business as ordinary income, through a W-2 salary or distributions taxed as self-employment income, you are handing the IRS a 30–40% cut before a single dollar gets to work for you. At a federal rate of 37% plus state taxes, a $100,000 distribution might land as $60,000 in your pocket. That’s the money available to invest, to compound, to become something in twenty years.

The entrepreneur down the street with a properly structured S-Corp, a Solo 401(k), and a defined benefit plan might be sheltering $80,000–$100,000 of that same $100,000 before taxes ever touch it. His compounding clock starts with $100,000. Yours starts with $60,000. Over 25 years at 8% annual growth, that difference compounds into $685,000 vs. $411,000, from a single year’s decision.

Do that wrong for ten years in a row, and you’ve destroyed millions in future wealth. Not because you didn’t earn enough. Because you paid the wrong people first.

Your entity structure is probably costing you real money

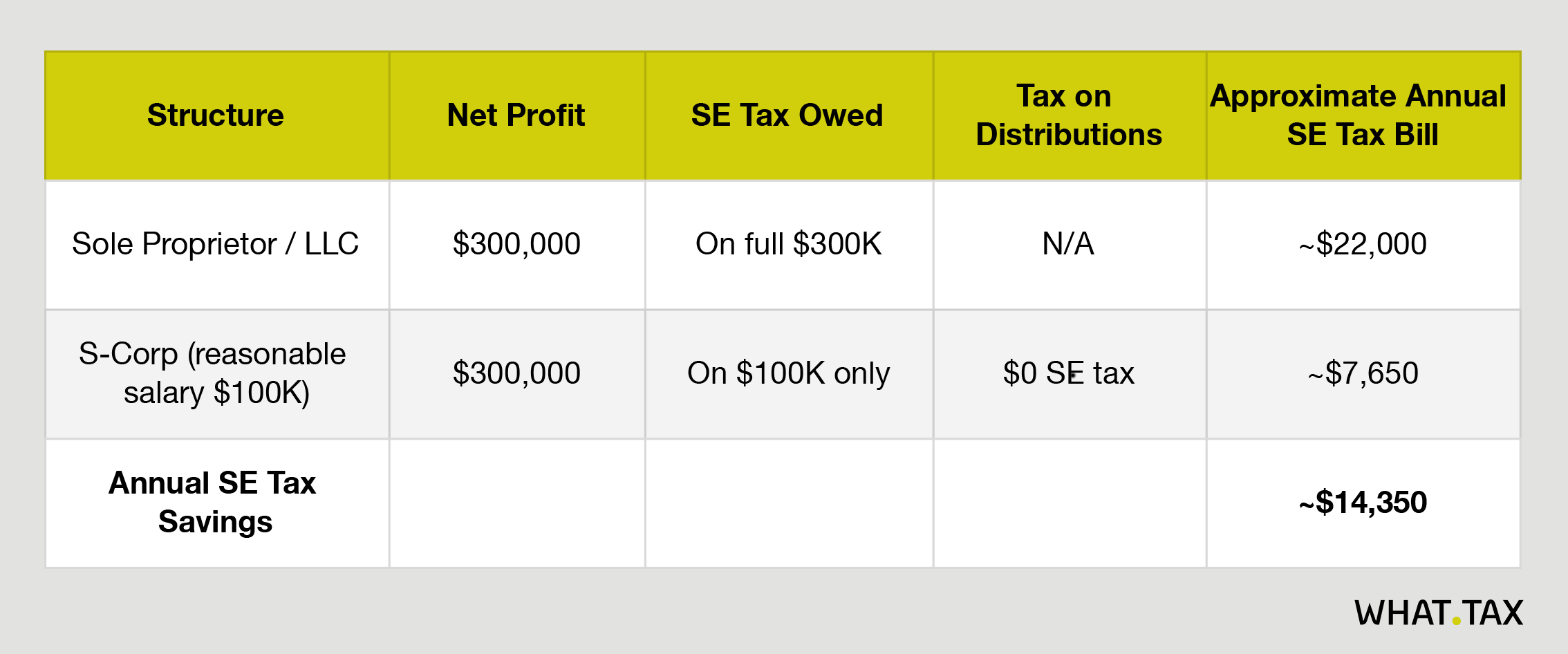

If you’re running a profitable business as a sole proprietor or single-member LLC and you haven’t elected S-Corp status, you are paying self-employment tax, currently 15.3% on the first $168,600 of net earnings and 2.9% above that, on every dollar of profit. That’s your money funding Medicare and Social Security for everyone else while your own retirement accounts sit empty.

The S-Corp election doesn’t eliminate this tax. It shrinks the base it applies to. The structure requires you to pay yourself a “reasonable salary”, subject to payroll taxes, and take the rest as a distribution that bypasses self-employment tax entirely. On $300,000 of net profit, a reasonable salary might be $100,000. You pay payroll taxes on $100,000 and pocket $200,000 as a distribution free of SE tax. That’s roughly $18,000 in annual savings that you can redirect into investments instead.

The setup costs a few hundred dollars with an accountant and a state filing fee. The payback period is measured in weeks.

This is not aggressive tax planning. It’s what the tax code explicitly allows. Failing to use it is leaving money on the table with a bow on it.

You’re ignoring the most powerful legal tax shelter in America

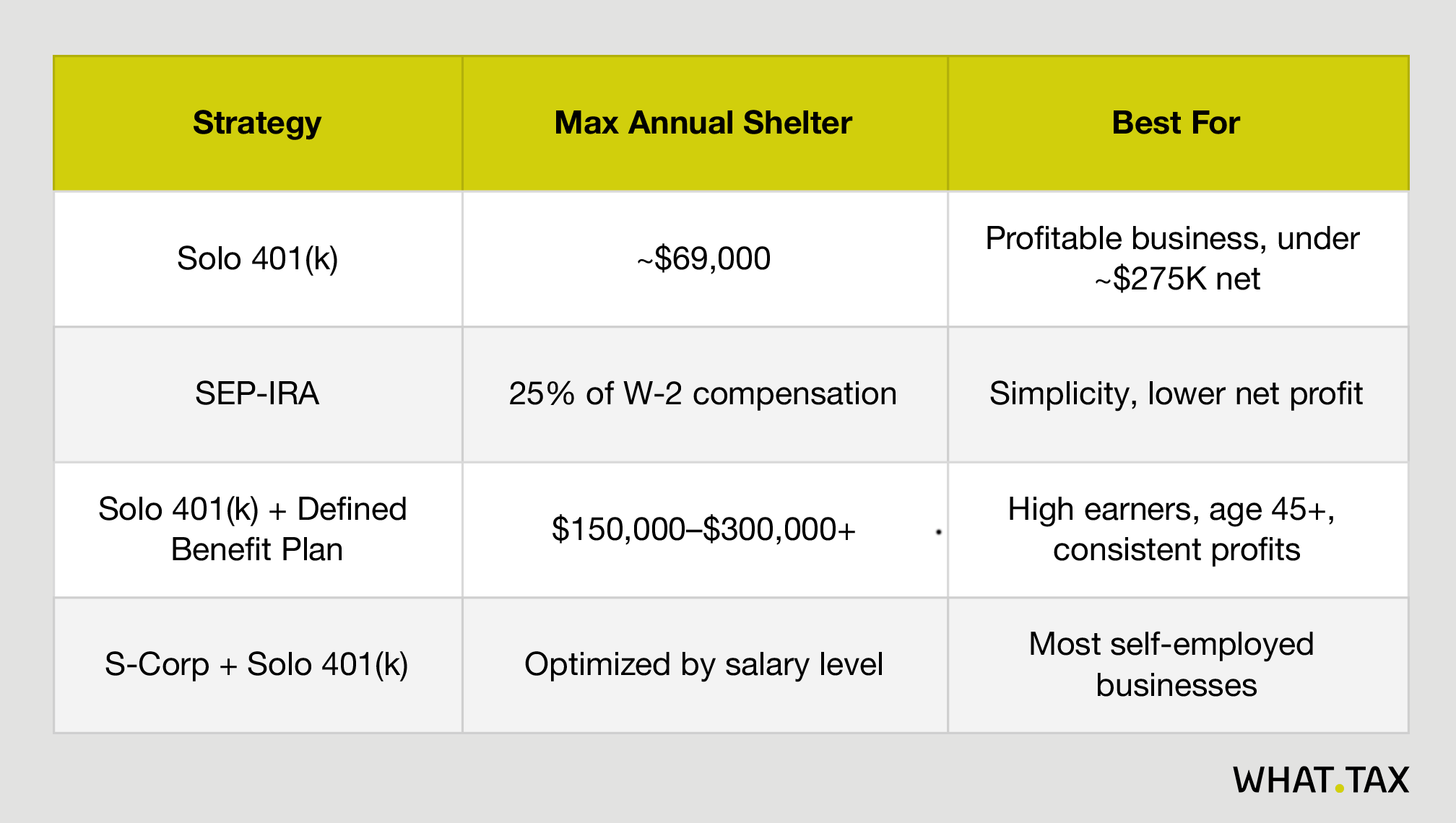

The Solo 401(k) is the single best retirement vehicle available to self-employed and small-business owners with no full-time employees (other than a spouse). In 2024, a business owner under 50 can contribute up to $69,000 annually. Over 50, the limit climbs to $76,500 with catch-up contributions.

Here’s how the math stacks up. As both employer and employee, you can contribute:

Employee deferral: up to $23,000 (or $30,500 if 50+)

Employer contribution: up to 25% of your W-2 compensation

On a $100,000 S-Corp salary, the employer side contributes $25,000. Add the employee deferral of $23,000. That’s $48,000 sheltered from income tax in a single year. Pre-tax, compounding, untouchable by the IRS until retirement.

Most entrepreneurs with Solo 401(k)s are using the pre-tax (traditional) version. But Roth Solo 401(k) contributions are also available for the employee deferral portion. If you believe your tax rate will be higher in retirement, or if you’re building toward a major liquidity event, paying tax now on $23,000 and letting it compound tax-free for 20 years can be worth far more than the upfront deduction.

The SEP-IRA is simpler to set up but is limited to the employer-side 25% contribution, with no employee deferral. At the same $100,000 salary, a SEP-IRA caps contributions at $25,000. The Solo 401(k) gets you nearly double. If you’re using a SEP-IRA out of habit, ask your accountant to run the numbers.

High earners: the defined benefit plan nobody talks about

If your business consistently earns $400,000 or more and you’re 45 or older, a defined benefit (DB) plan can shelter more income than most people think is legal. These are old-school pension-style plans, and the IRS contribution limits are based on age and projected benefit, not a flat-dollar cap.

A 50-year-old business owner can potentially shelter $200,000 or more per year in a properly structured DB plan combined with a 401(k). The contributions are actuarially determined and must continue each year, requiring commitment and cash-flow predictability. But for the right business owner, this is the fastest legal way to compress decades of wealth-building into a shorter window.

The cost to administer, typically $2,000–$5,000 per year in actuarial and plan fees, is trivial against the tax savings. A $200,000 pre-tax contribution for someone in the 37% bracket saves $74,000 in federal income tax alone. One year.

The business is not your retirement plan

This is the sentence that most entrepreneurs read, nod at, and then ignore entirely.

You’ve built something valuable. Maybe it will sell for a great multiple one day. But a business that hasn’t been formally valued, has no documented systems, is dependent on your personal relationships, and has never been through a third-party audit is worth exactly what someone will pay for it on the day you decide to sell, not what you imagine it’s worth while you’re running it.

Businesses sell for 3x–10x earnings in most service industries. Some SaaS or product businesses command more. But a solo-dependent consulting firm, a personal brand business, a professional practice where the relationships walk out with the owner, these are some of the hardest businesses to sell at premium multiples, because buyers are purchasing risk.

Meanwhile, a diversified investment portfolio in index funds and real estate doesn’t have key-man risk. It doesn’t have a Yelp page. It doesn’t depend on your health.

The entrepreneur who pours every dollar back into the business, treats the business as an ATM for lifestyle, and defers all external investing until the “big exit” is taking a bet with no hedge. Some of those bets pay off spectacularly. Most don’t. The ones that do often pay off on a timeline that felt punishing on the way there.

Building parallel wealth while running a profitable business is not a distraction. It’s insurance against your own exit.

The lifestyle creep problem nobody admits

When money gets easy, spending follows. This is not a moral failure; it’s human nature, and it’s almost universal. The upgrade cycle is real: the car, the house, the team, the travel, the tools, and anything that feels justified because the revenue supports it.

The problem is that higher lifestyle spending raises your personal burn rate while lowering the capital available for investment. A business owner spending $250,000 per year on personal expenses has to earn $400,000+ before taxes just to sustain that lifestyle. Every dollar saved from lifestyle reduction goes directly into your compounding base.

The fix isn’t austerity. It’s intentionality. Decide what your “enough” number is for annual personal spending. Pay yourself that number, no more, no less, and treat every dollar above that as investment capital. Give it a destination before it hits your personal checking account. This is the same principle that makes payroll automatic: money that leaves before you see it doesn’t get spent.

A practical version of this: pay yourself a fixed monthly owner distribution, set it up like a paycheck, and route all excess profit into a separate investment account that you treat as off-limits for anything other than investing. This takes about 30 minutes to set up with your bank and immediately changes your relationship with business income.

What “building wealth” actually looks like in practice

It’s not complicated, but it is specific. Here’s what a profitable entrepreneur’s financial structure should look like:

First, optimize the entity. If you’re net-profitable above $50,000 and not an S-Corp, make the election. Second, establish a Solo 401(k), this should exist before you spend another dollar on anything discretionary. Third, set a reasonable salary through your S-Corp that maximizes your 401(k) employer contribution without triggering unnecessary payroll taxes. Your accountant should be running this optimization annually, not just at tax time.

Fourth, if you’re consistently profitable above $300,000 and over 45, explore a defined benefit plan with an actuary. The upfront cost of a conversation is zero. Fifth, establish a taxable brokerage account, Vanguard, Fidelity, Schwab, pick one, and automate a monthly contribution from your operating account. The amount matters less than the habit. Sixth, consider real estate, but only when you have liquidity. Real estate is not a substitute for liquid investments; it’s a complement to them, and illiquid real estate owned by a cash-strapped business owner is just another liability.

None of this requires complexity. It requires decisions.

The real question

You built a profitable business. That took skill, risk, sacrifice, and years. The fact that your P&L looks good is not to be taken lightly; most businesses fail.

But profit is an input to wealth, not wealth itself. The entrepreneurs who end up financially free aren’t necessarily the ones who earned the most. They’re the ones who built a parallel financial structure that captured, sheltered, and compounded a portion of what they earned every year, through good years and bad ones.

The gap between your revenue and your net worth is not your accountant’s fault, and it’s not the IRS’s fault. It’s a structural gap that was never deliberately closed.

Close it deliberately. Start with one decision this week: the S-Corp election, the Solo 401(k) application, or the conversation with your accountant about contribution limits. One decision compounds into the next.

The business is doing its job. Now build the machine that works for you.

The information in this newsletter is for educational purposes only and does not constitute tax or legal advice. Work with a qualified CPA or tax attorney to evaluate strategies specific to your situation.

Found this useful? Give it a like or share it with an entrepreneur who’s still treating taxes like an April problem.

This is a really eye-opening article highlighting a key point many entrepreneurs miss: it’s not just about earning income, but about building wealth over time. I also love the idea of creating wealth alongside running a business—it’s easy to forget about long-term planning when you’re focused on growth.