The Roth Conversion Window That Could Save High Earners $150K in Retirement Taxes

Why permanent TCJA rates didn’t kill this strategy. They sharpened it.

For a decade, the Roth conversion pitch ran on borrowed urgency. Convert before the TCJA sunsets in 2026, or pay 39.6% later.

That talking point died on July 4, 2025, when the One Big Beautiful Bill Act made the seven-bracket structure permanent. The top federal rate stays at 37%. The 22% and 24% brackets keep their generous widths. No legislative cliff is coming.

Most newsletters concluded: panic over, move on.

That’s the wrong read. The window for Roth conversions never had much to do with Congress in the first place. It has to do with the gap between your top-earning years and the year RMDs start dragging mandatory income onto your 1040.

Permanent rates didn’t eliminate that gap. They froze it in place at historically low levels and handed entrepreneurs a stable runway to plan against. The advisors I respect spent the last six months rebuilding their conversion playbooks around this reality. Most subscribers haven’t.

If you’re an entrepreneur with a fat traditional 401(k), a SEP IRA, or a rolled-over deferred comp account, here’s what’s on the table:

$150,000 in lifetime federal tax savings is a conservative estimate

With Medicare surcharges and survivor-bracket effects layered on, the real number for many readers will clear $200K

The strategy compounds: every year you delay is a year of growth inside your highest-tax bucket

Below is the framework, the math, and the three mistakes that quietly burn most of the savings.

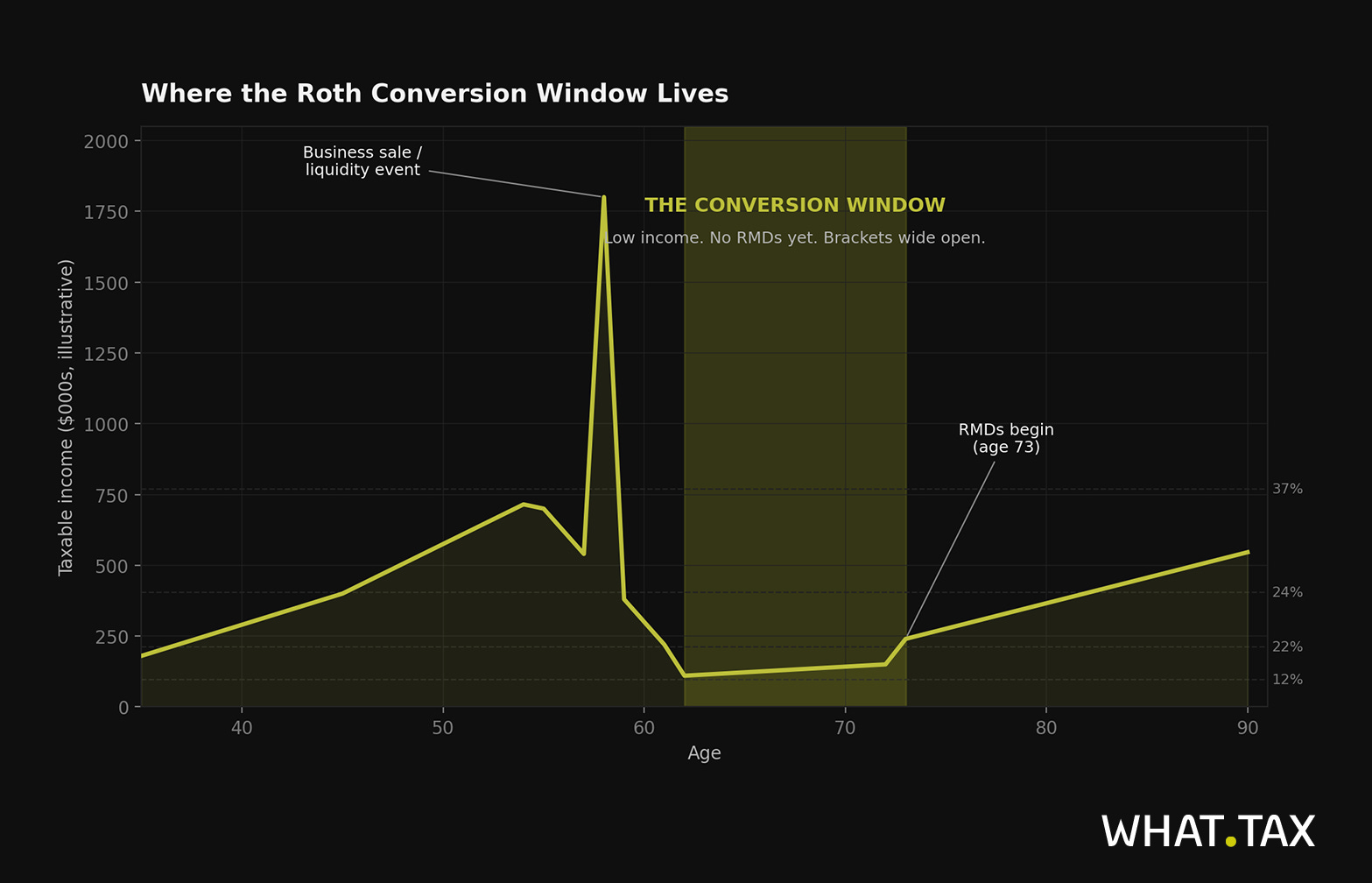

What “the window” actually means now

Forget the legislative angle. The window is a personal one, defined by three forces converging on a small number of years:

Your taxable income drops. You sold the business, took a sabbatical, restructured comp around K-1 distributions instead of W-2 wages, or stepped back from operations. Entrepreneurs see this volatility constantly. Salaried executives don’t.

Social Security hasn’t started yet. Every dollar of provisional income you avoid in your 60s is a dollar you can convert at a marginal rate you choose, rather than one the IRS chose for you. Delaying Social Security to 70 widens the conversion runway by eight years and bumps the eventual benefit by 32%.

RMDs aren’t pulling money out of your traditional accounts. SECURE 2.0 sets the start age at 73 for anyone born between 1951 and 1959, and 75 for those born in 1960 or later. Until you hit that age, you decide what comes out and when. After that, the IRS sets the floor.

Stack those three together, and you get the Roth conversion window. For most founders and operators, it opens between ages 55 and 65 and closes the year RMDs begin. In some cases, it lasts fifteen years. In others, three.