Founders Get One Shot at Section 1202. Most Use It Wrong.

The tax code hands founders a $15M federal exemption on exit gains. The requirements are strict, the traps are silent, and most entrepreneurs only find out they failed after the deal is already signed

Section 1202 of the Internal Revenue Code is not a loophole. Congress wrote it deliberately, with one goal: to reward founders and early investors who build real, operating U.S. businesses over the long term. When it works, the benefit is extraordinary. A founder can sell their company and pay $0 in federal capital gains tax on up to $15 million in profit. With the right planning structure, that number can climb well past $60 million across a single family.

When it doesn’t work, there’s no partial credit. No consolation prize. The exclusion is binary, and the mistakes that kill it are almost always invisible until the moment of exit, when it’s too late to fix them.

Most founders hear about Section 1202 at formation, nod along, and then treat it like a background feature. They don’t touch it again until the term sheet arrives. That is the mistake. Section 1202 is not a checkbox at formation. It’s an ongoing compliance obligation that runs for the entire holding period, and it’s far more fragile than any attorney will typically tell you in a 30-minute onboarding call.

Here, we cover what the rule actually says, what just changed in 2025, where founders quietly destroy their eligibility, and what the real planning opportunity looks like for those who get in front of it.

What Section 1202 Actually Does

Section 1202 allows a non-corporate taxpayer to exclude up to 100% of federal capital gains tax on the sale of Qualified Small Business Stock (QSBS), held for the required period, up to a cap of the greater of $15 million or 10 times the shareholder’s adjusted basis in the stock.

That “10x basis” alternative matters more than most people realize. If you founded your company and received stock for $100,000 in cash or services, your basis might be near zero. The $15 million cap will govern. But if you invested $2 million as an early investor, the 10x test gives you a $20 million exclusion ceiling instead, which exceeds the flat cap. Investors with a meaningful basis should always run both calculations before assuming the $15 million figure.

The exclusion eliminates not just the 20% long-term capital gains rate but also the 3.8% Net Investment Income Tax (NIIT). Combined, the federal tax rate on QSBS gains can go from 23.8% to zero. On a $10 million gain, that’s $2.38 million in tax that disappears entirely.

States are another matter. California famously does not conform to the federal QSBS exclusion. Residents of California, Pennsylvania, Alabama, Mississippi, New Jersey (until very recently), and a handful of other states owe state tax on those gains even when the federal bill is zero. New Jersey enacted conformity in mid-2025, which is a meaningful development for founders there, but California remains the most painful outlier.

The One Big Beautiful Bill Act Changed the Rules in July 2025

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act into law, and Section 1202 got its most significant expansion since 2010. If you have stock issued after July 4, 2025, the rules are materially different from what came before. If your stock predates that day, the old rules still govern it entirely.

Here’s what changed:

The gross asset cap increased from $50 million to $75 million, with inflation indexing starting in 2027. This matters because many companies lost QSBS eligibility the moment a funding round pushed aggregate gross assets past the old $50 million ceiling. A company that had $48 million in assets at its Series A but exceeded $50 million after the round closed could not issue new qualifying shares to incoming investors. The new $75 million threshold opens the window for more late-seed and Series A companies.

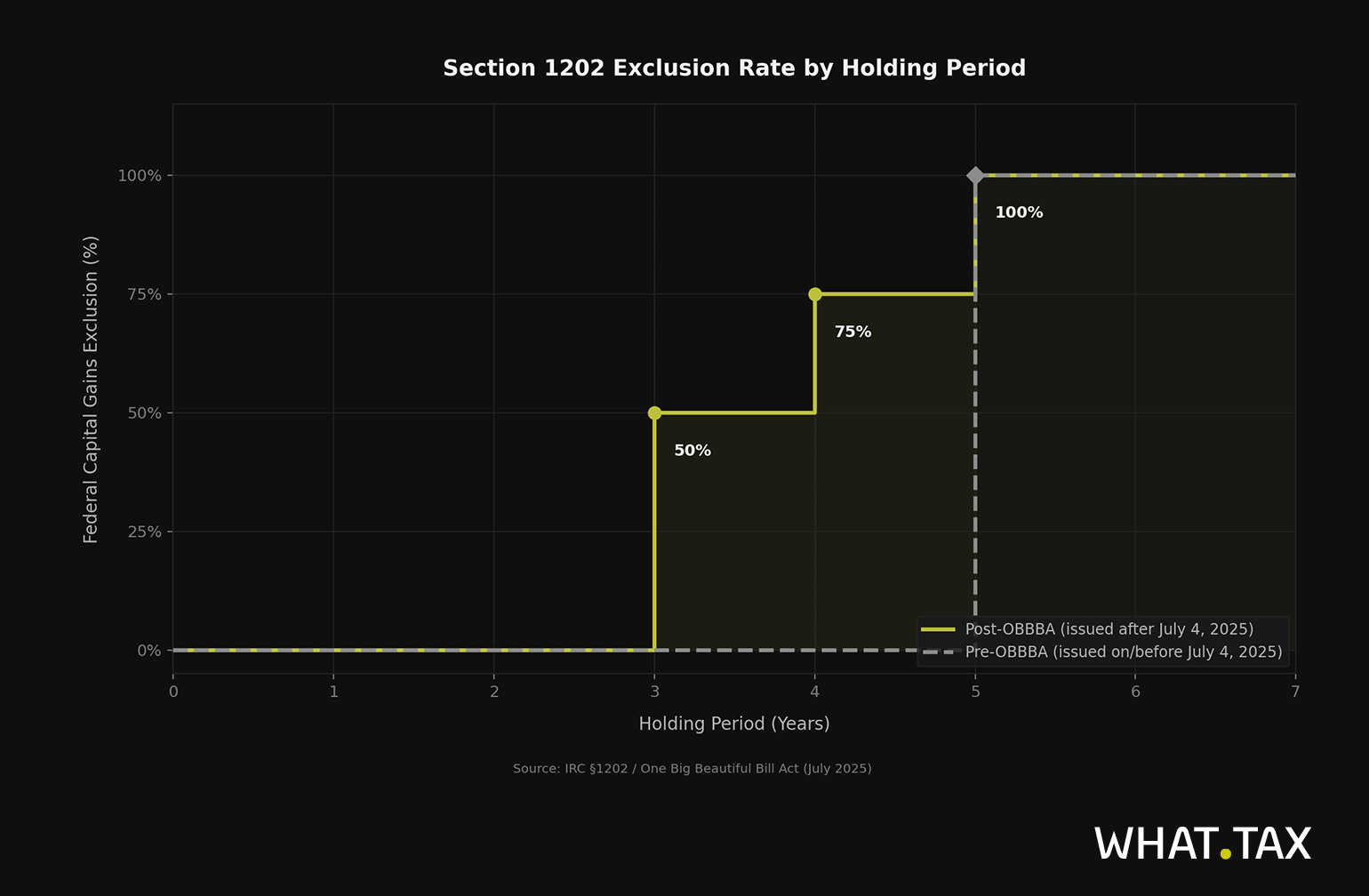

The holding period requirement dropped from five years to three, but with a tiered structure. Stock issued after July 4, 2025, now qualifies for a 50% exclusion after three years, 75% after four years, and the full 100% after five years. This is not purely good news. The gain that is not excluded under the three- and four-year tiers is taxed at 28%, rather than the standard long-term capital gains rate of 20%. Founders who sell at the three-year mark, thinking they’ve “mostly made it,” may be surprised to find the taxable portion costs more than expected.

The per-taxpayer exclusion cap rose from $10 million to $15 million for stock acquired after July 4, 2025. Stock acquired on or before that date is permanently subject to the $10 million cap, even if sold years from now.

The chart above illustrates how this tiered structure compares to the old all-or-nothing rule. Pre-OBBBA stock required a full five-year cliff. Post-OBBBA, stock builds up incrementally, creating more planning flexibility but also new traps for founders who assume early liquidity is now clean.

The Checklist Nobody Reads Until It’s Too Late

There are five core requirements for stock to qualify under Section 1202. Most founders know one or two. Missing any single one eliminates the exclusion entirely.

1. The corporation must be a domestic C corporation

Not an S corporation. Not an LLC taxed as a partnership. Not an LLC that elected S-corp status. The issuing entity must be a C corporation at the time the stock is issued and remain a C corporation. An S election after incorporation is one of the most reliable ways to destroy QSBS status. The switch is irrevocable for the purposes of the exclusion on any stock issued while the company was an S corp.

LLCs that convert to C corporations can begin issuing qualifying stock after conversion, but the conversion date starts the clock. Any equity issued before conversion does not qualify. Founders who spent two years building as an LLC before formalizing into a C corp should verify exactly when each share was issued relative to the conversion date.

2. The gross asset test must be satisfied at issuance

At the time your stock is issued (and immediately after, taking into account any proceeds received), the corporation’s aggregate gross assets must not exceed $50 million (or $75 million for stock issued after July 4, 2025). This is a point-in-time test, not a rolling average. Once stock is issued within the threshold, subsequent growth does not retroactively disqualify it.

However, every new share issuance triggers a fresh test. When a company raises a Series B and issues new shares to investors, those new shares must be tested against the gross asset limit on their issuance date. A Series A investor whose shares were issued when gross assets were $30 million is fine. A Series B investor whose shares were issued when gross assets sat at $55 million (pre-OBBBA) has stock that never qualifies.

Large fundraising rounds are the most common mechanism for pushing a company over the threshold. Founders should run the gross asset calculation before every round closes, not after, because post-closing is too late.

3. The stock must be acquired at original issuance

This requirement disqualifies a significant category of transactions that founders and early employees often overlook. Secondary purchases of shares, stock acquired in open-market-style transfers from another shareholder, and shares received through certain reorganizations do not qualify. The stock must come directly from the corporation itself, not from a selling founder or employee.

The implications are practical and often counterintuitive. If an early employee sells you their shares directly, you don’t have QSBS. If a founding team member distributes shares to a partner after formation, the circumstances matter. Corporate redemptions within certain windows surrounding the issuance date can also taint newly issued shares under anti-abuse rules, even when the redemption involves different shareholders and share classes.

4. The active business test must be met continuously

At least 80% of the corporation’s assets must be used in the active conduct of a qualified trade or business for substantially all of the shareholder’s holding period. This is the requirement that founders most frequently underestimate because it doesn’t feel like a one-time event. It isn’t.

When the company raises a large round and sits on a cash balance waiting to deploy it, that idle cash counts as a non-active asset. A company that closes a $20 million Series A and deploys it over 18 months is running a real risk of failing the 80% test during that deployment window.

Late-stage pivots are another common disqualifier. A SaaS company that spins up a professional services arm, a medtech company that starts running clinical operations, a fintech that begins offering regulated financial products directly: all of these can shift the asset base in ways that slip below the 80% threshold. The IRS will look at the substance of where revenue and assets actually live, not how the company describes itself on its website.

5. The business must operate in a qualified industry

Congress wrote a specific list of disqualified industries into the statute, and it’s broader than most founders expect. Professional services in health, law, engineering, accounting, and consulting are excluded. So are financial services, banking, insurance, leasing, and investing. Hospitality is excluded. Farming, mineral extraction, and oil and gas are out.

The “principal asset is the reputation or skill of employees” rule catches a wide range of businesses that don’t neatly fit into one of the named categories. A boutique consulting firm that happens to have built software doesn’t automatically become a qualified tech company. A clinical research organization where the value is researcher expertise doesn’t qualify just because it uses SaaS tools. The IRS looks at where the economic value is actually generated, and that analysis is fact-intensive and sometimes contested.

The gray zone that generates the most disputes is “consulting.” Many businesses involve some form of customer-specific implementation, customization, or advisory services alongside a core product. Whether that tips a company into the disqualified consulting category depends on how revenue is generated, how assets are used, and how contracts are structured.